The Chinese century: how Beijing is reshaping the world’s technology, industry and influence

From factory floors to artificial intelligence, from African ports to outer space — China’s rise is no longer a forecast. It is a fact being assembled in real time.

By Diaspora Times Team

China has quietly, systematically, and with extraordinary deliberation positioned itself as the dominant force in global manufacturing, technology, and geopolitical influence — a transformation so comprehensive in scope that it is reshaping the world order faster than most Western governments have been willing to acknowledge.

The numbers alone tell a story that is difficult to argue with. In 2025, China contributed approximately 30 percent of global manufacturing added value, maintaining its position as the world’s largest manufacturing power — a title it has held for well over a decade and shows no signs of surrendering. A new report from the Information Technology and Innovation Foundation published in May 2026 found that China now produces nearly one quarter of global output across the world’s most advanced industries, extending its lead over the United States and other major economies across high-value, innovation-driven sectors. These are not the numbers of a developing nation catching up. They are the numbers of a country that has already arrived and is now setting the pace for everyone else.

To understand how China got here requires looking beyond the headline figures to the structural choices made over decades. China’s manufacturing output climbed from roughly $134 billion in 1980 to roughly $4.8 trillion in 2023. During that time, China’s share of global manufacturing output climbed from 5 percent to around 30 percent, while the United States saw its share drop from 21 to 17 percent. The United States peaked at 28 percent in 2001 — the same year China joined the World Trade Organisation. What followed was not a coincidence. It was the consequence of a deliberate, state-backed industrial strategy that identified manufacturing dominance as the foundation upon which every other form of national power could be built.

That model is underpinned by massive state support. Beijing channels billions into subsidies, low-interest government loans, tax incentives, and strategic investments, allowing Chinese firms to operate profitably on razor-thin margins and keeping prices aggressively competitive worldwide. Critics in Washington, Brussels, and Tokyo call this unfair competition. Beijing calls it industrial policy. The distinction matters less than the outcome: Chinese goods dominate global supply chains in ways that competitors have spent years trying, and largely failing, to replicate.

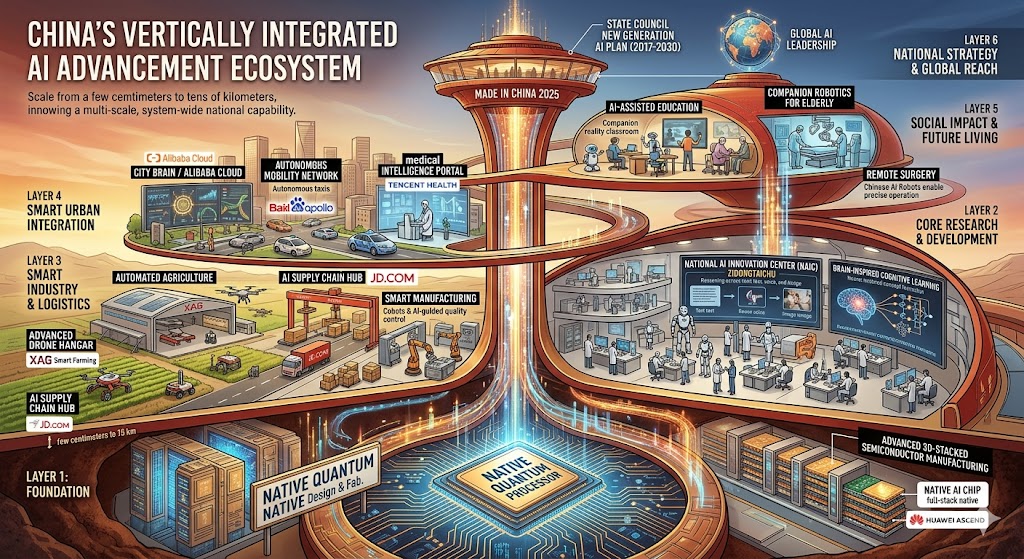

But the most important shift in China’s global position is not about cheap goods or high volume. It is about the transition from manufacturing muscle to technological leadership — a move that is already well advanced and accelerating. According to research tracking 74 critical technologies globally, China leads in 66 of them — a statistic that captures a tectonic shift in how China leads, moving beyond manufacturing into innovation itself. Once known primarily for scaling production, China’s research institutions now dominate fields including high-performance computing, artificial intelligence hardware, and quantum communications.

In artificial intelligence, the race is closer than American commentators tend to acknowledge, but China’s trajectory is unmistakable. Chinese AI advancement accelerated sharply in early 2026, with multiple flagship model releases from leading technology companies. Alibaba unveiled Qwen3-Max-Thinking, claiming performance comparable to leading Western models. Moonshot AI released Kimi K2.5, positioning it as among the world’s most powerful open-source models. These releases did not emerge from nowhere. They are the product of a research ecosystem built over years through coordinated state investment, a vast pool of engineering talent emerging from Chinese universities, and data access at a scale that few other countries can match given China’s 1.4 billion population.

China’s 15th Five-Year Plan, covering 2026 to 2030, prioritises advanced logic chip processes, memory expansion, and equipment localisation — a direct response to American export controls on advanced semiconductors that sought to slow China’s technological ascent. The controls have had some effect, but they have also accelerated China’s drive toward self-sufficiency in chip manufacturing, a goal Beijing now pursues with the urgency of a national security imperative. The Semiconductor Manufacturing International Corporation continues producing at advanced nodes using domestic equipment, and investment in the sector has reached levels that suggest China intends to close the gap regardless of cost.

In electric vehicles, China has already won the first round. BYD delivered 2.26 million battery-electric vehicles in 2025, surpassing Tesla’s 1.64 million to become the world’s leading EV manufacturer. That figure would have been inconceivable to American and European automotive executives a decade ago, when China’s EV ambitions were still dismissed as aspirational. Today, BYD operates in dozens of international markets, with export momentum remaining strong — 100,482 vehicles exported in January 2026 alone, a 51.4 percent increase year on year, with a 2026 target of 1.3 million overseas sales. Meanwhile, more than 50 car brands in China now use ByteDance’s Doubao AI model embedded in vehicles, with the technology deployed across 145 car models and over 7 million vehicles. The car is no longer just a vehicle. In China, it has become a rolling artificial intelligence platform.

China’s Ministry of Industry and Information Technology released its 2026 automotive standardisation work plan in May, outlining measures to tighten technical requirements for electric vehicles, AI systems in automated driving, automotive chips, battery safety, and solid-state batteries — effectively positioning China to set the global standards in the industry it now leads. Whoever sets the standards in a dominant industry writes the rules for everyone else. China understands this. Its competitors are only beginning to.

Economically, the full picture is more nuanced than either China’s champions or its detractors typically allow. China’s economy grew 5.0 percent in the first quarter of 2026 compared with a year earlier — a solid performance, though one achieved against significant headwinds including a property sector still working through years of excess debt, a population that is ageing faster than anticipated, and domestic demand that has not yet fully recovered its pre-pandemic dynamism. China’s GDP reached $19.63 trillion in 2025, compared to the United States’ $30.77 trillion — a gap that has not closed as rapidly as many forecast in the early 2020s. The Centre for Economics and Business Research, which in 2020 predicted China would overtake the US by 2028, revised that forecast to 2036. Some economists now question whether it will happen at all in nominal dollar terms.

Economically, the full picture is more nuanced than either China’s champions or its detractors typically allow. China’s economy grew 5.0 percent in the first quarter of 2026 compared with a year earlier — a solid performance, though one achieved against significant headwinds including a property sector still working through years of excess debt, a population that is ageing faster than anticipated, and domestic demand that has not yet fully recovered its pre-pandemic dynamism. China’s GDP reached $19.63 trillion in 2025, compared to the United States’ $30.77 trillion — a gap that has not closed as rapidly as many forecast in the early 2020s. The Centre for Economics and Business Research, which in 2020 predicted China would overtake the US by 2028, revised that forecast to 2036. Some economists now question whether it will happen at all in nominal dollar terms.

Yet the nominal GDP comparison, while important, captures only part of the story. The IMF forecasts China will contribute 26.6 percent of global real GDP growth in 2026 — by far the largest share of any country. China ranks first among all nations in total GDP added over the period 2026 to 2030, projected to expand by $5.7 trillion, ahead of the United States at $5.0 trillion. In terms of purchasing power parity — which adjusts for the fact that a dollar buys far more in China than in New York — China’s economy is already larger than America’s and has been for years. For the billions of people in developing countries who trade with China, it is those purchasing-power-adjusted realities that determine the relationship, not the nominal dollar comparison that preoccupies Western commentators.

It is in the developing world where China’s influence is most visibly and rapidly expanding. In 2025, Belt and Road Initiative engagement reached record levels — $128.4 billion in construction contracts, an 81 percent increase from 2024, and $85.2 billion in investment, a 62 percent increase — with total cumulative BRI engagement reaching $1.399 trillion since 2013 across 150 countries. The BRI’s critics, concentrated in Western capitals, describe it as debt-trap diplomacy — a strategy of building infrastructure in exchange for strategic leverage over indebted governments. Its supporters, more numerous in the Global South, describe it as the only major international infrastructure financing programme willing to build roads, railways, and ports in places that Western development banks have long declined to fund.

Africa’s trade with China reached a record $275 billion in 2024, with the continent importing $182 billion in Chinese goods. China is Africa’s largest trading partner by a substantial margin, and its presence on the continent — through construction projects, manufacturing investment, telecommunications infrastructure, and development finance — gives Beijing a relationship with African governments and populations that Washington has consistently underestimated and only recently begun to take seriously. As African nations navigate the transition to clean energy, Chinese manufacturers of solar panels, batteries, and electric vehicles are positioning themselves as the primary suppliers — deepening economic ties that are likely to persist for generations.

The comparison with other major powers reveals the scale of China’s advantage. The United States remains ahead in nominal GDP, dominates in financial services, leads in biotechnology and medical research, and retains unmatched military projection capacity. Its universities continue to attract the world’s best researchers, many of them Chinese, and its technology companies still define the global software landscape. But in manufacturing, in infrastructure investment, in clean technology, and in the depth of its industrial ecosystems, the United States has ceded ground that will be extraordinarily difficult to recover. Europe faces a similar reckoning. Germany’s automotive industry — once among the world’s most formidable — is confronting a structural threat from Chinese EV manufacturers that its own government has been slow to address. Japan and South Korea remain strong in specific sectors but lack the scale and state capacity to mount a comprehensive response to Chinese industrial ambition.

India is frequently cited as the country best positioned to challenge China’s manufacturing dominance over the coming decades, and there is genuine substance to that argument. India’s working-age population will surpass China’s in absolute terms within this decade, its democratic institutions provide a degree of political legitimacy that China’s authoritarian model cannot match in Western eyes, and its technology sector has demonstrated genuine world-class capability. But India’s infrastructure deficit, regulatory complexity, and the sheer time required to build the kind of industrial ecosystem China has spent forty years constructing mean that the competitive challenge India poses remains a projection rather than a present reality.

The more honest assessment is that China is not simply leading in any single domain. It is building a self-reinforcing system in which manufacturing scale funds research investment, research investment generates technological leadership, technological leadership enables export dominance, export dominance finances Belt and Road infrastructure, and Belt and Road infrastructure creates the political relationships that insulate China from the consequences of Western pressure. That system is not without its vulnerabilities — demographic decline, property debt, and the political costs of authoritarian governance are real constraints. But they are constraints on the pace of China’s rise, not on its direction.

The world that China is building, piece by piece, port by port, patent by patent, is one in which the centre of gravity in technology, industry, and influence tilts steadily eastward. The question for every other nation is not whether that shift is happening — it is — but how quickly they are willing to recognise it and what, if anything, they intend to do in response.

China is not waiting for the answer.

Similar Posts by The Mt Kenya Times:

- Political goonism is becoming a national security threat

- Imenti North MP defends development record, urges support for Kinoru projects

- Flipping the rulebook: Women thriving in careers once reserved for men

- Motorsport queen Pauline Shegu nominated for top international award

- World Cup final set: Spain and Argentina book their place